Fabby Tumiwa is executive director of the Institute for Essential Services Reform, an energy and environmental policy think tank in Jakarta, and chairman of the Indonesian Solar Energy Association. Marlistya Citraningrum is program manager for sustainable energy access at the institute and managing director of its SolarHub information portal.

With countries racing to reduce emissions by increasing their use of renewable energy, the geopolitics of energy is shifting toward countries and regions with a competitive edge in clean technologies.

China’s dominance in many clean technologies has prompted the U.S. to adopt legislation to incentivize domestic manufacturing, most importantly the Inflation Reduction Act, which will channel up $400 billion in funding toward clean energy, with priority given to users of domestic components.

This kind of protectionist policy has raised concerns in many countries. The EU is now developing a comparable package.

What does this trend mean for Southeast Asia, a region of rapidly growing emerging economies committed to do their own part in addressing climate change?

Following the success of Indonesia’s presidency of the Group of 20 last year, Jakarta has adopted the theme “Epicentrum of Growth” as the 2023 chair of the Association of Southeast Asian Nations, focusing on strengthening the region as a fast-growing, inclusive and sustainable economic area, particularly in terms of health architecture, food and energy security, and financial stability.

ASEAN has yet to cement its clean energy leadership, but notable progress has been made in terms of pledges and installations.

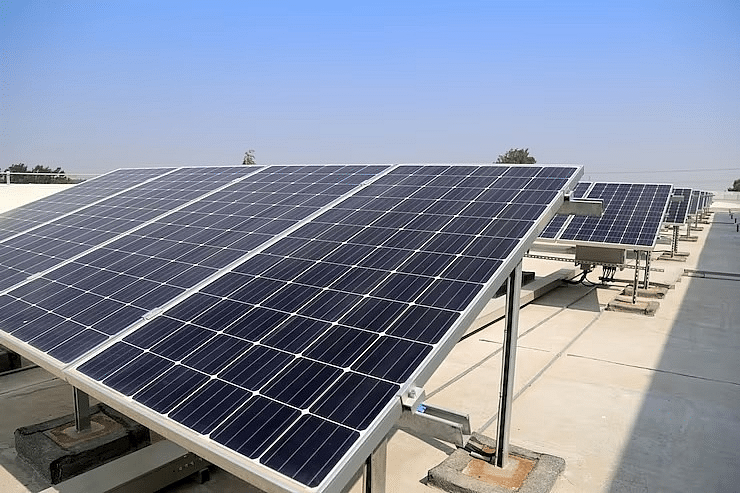

Solar energy has entered mainstream policy in most ASEAN member states. As the front-runner, Vietnam added almost 20 gigawatts of solar energy capacity in only four years with the help of favorable guaranteed prices for power producers. Thailand is second with 3 GW of solar, while Indonesia is lagging, with less than 1 GW. Vietnam has also made notable progress with wind power.

Southeast Asia currently has annual capacity to produce 69 GW worth of solar power modules and the components to make them, according to McKinsey & Co. Thailand, Vietnam and Malaysia together account for about 10% of global solar cell and module production.

It is worth noting that much of this production is controlled by Chinese companies. The region still lacks the capability to produce polysilicon or wafers, which still tend to be imported from China.

The capacity gap, though, is attracting interest from global investors.

California-based SEG Solar recently signed an agreement with China’s Jiangsu Meike Solar Technology, a leading silicon wafer maker, to establish a cell manufacturing base in Southeast Asia. The Indonesian Ministry of Investment said in June that SEG Solar will also team up with local company ATW Solar Indonesia to build a $500 million solar cell and module factory in Central Java that will be the first of its kind in the country.

ASEAN’s record in regional cooperation in this area is not very impressive.

Plans for an ASEAN Power Grid have been around since the 1990s but there has so far been only a minuscule amount of energy exchanged and energy trading has progressed even more slowly.

The ASEAN Plan of Action for Energy Cooperation, meanwhile, has been criticized as an “accumulation of country-level energy plans” rather than a real regional strategy. It should be noted too that Malaysia and Indonesia banned renewable electricity exports to neighboring Singapore in 2021 and 2022, respectively, suggesting a prioritization of national energy security over bloc interests.

A production line for solar PV components at a factory in Zhejiang province, China in 2019: Demand for solar PV modules is set to rise rapidly in Southeast Asia. (Zhejiang Daily via Reuters)

The tide, though, may be turning toward a more regional approach. In March, Singapore and Indonesia signed a pact focused on green energy industrial cooperation. The partnership includes a plan to build a floating solar farm with multiple gigawatts of capacity in Indonesia’s Riau Islands near Singapore, as well as solar cell and module factories. Singapore has also secured a clean energy trade agreement with Cambodia.

More of this type of cooperation will be needed to boost ASEAN’s solar leadership, including technology exchanges, investment facilitation and collaboration to expand exports to other countries and regions.

Every ASEAN member state has pledged to reach net-zero emissions by 2050 or 2060. Solar power generation is beginning to take off. Global investors are seeking to put money into projects in the region.

But coordinated efforts are still lacking. To take the region’s power system forward, it will be important to ensure solid grid interconnectivity between member countries and to increase storage capacity and power system flexibility to accommodate more solar energy.

Regional demand for solar photovoltaic (PV) modules is set to rise rapidly. The International Renewable Energy Agency estimates that Southeast Asia will need to install 240 GW of solar energy by 2030; it now has about 24 GW of solar capacity.

To ensure the security of solar cell and PV module supplies, Southeast Asian nations should be working together to make the region a production hub. Indonesia and Malaysia could supply the needed metallurgical-grade silicon to produce silicon wafers and ingots; the cells and modules themselves could be made anywhere in the region, building on the comparative advantage of each country’s existing industries.

ASEAN energy ministers are due to meet this week in Bali. It is important that they seek agreement to advance regional cooperation while setting a timetable for implementation. Solar industry cooperation can be a real and tangible outcome of Indonesia’s chairmanship and provide timely support for the region’s energy transition.

Source: https://asia.nikkei.com/Opinion/ASEAN-can-be-a-power-in-solar-energy-with-teamwork